RPN-38 — Cash-Flow Calculations

|

Introduction

Cash-flow calculations on the HP-38 are used to solve financial problems where cash flows occur at regular intervals but are of varying amounts. You can also use cash-flow calculations to solve problems with regular, equal, periodic cash flows, but these situations are handled more easily using the TVM application.

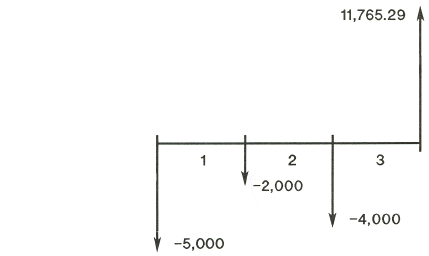

A Short Term Investment The following cash-flow diagram represents an investment in stock over three months. Purchases were made at the beginning of each month, and the stock was sold at the end of the third month. Compute the internal rate of return.

|

|

Computing Net Present Value (NPV)

The net present value function is used to discount the cash flows in the list to the front of the time line using a periodic interest rate that you supply.

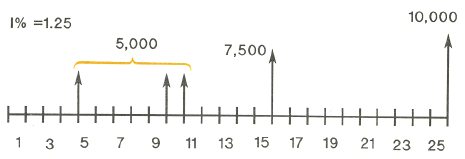

Example: You have been offered a chance at purchasing a contract with the following cash flows.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

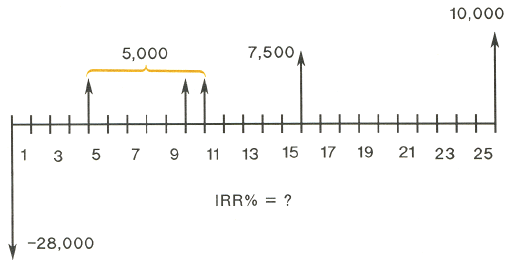

Computing Internal Rate of Return (IRR)

The following example uses the cash-flow list that was keyed in when you worked the previous NPV example.

Example: If the seller of the contract in the

previous example wants $28,000 and you accept that price, what is your yield?

When you compute NPV, the result is stored in PV for your convenience. To recall that result, tap RCL PV. If you haven't changed any of the TVM values since you worked the last example using NPV, pressing RCL PV should display PV = 27,199.92. When you compute IRR, the result is stored in i. Tapping RCL g i after working this example will display 12.49. This is the annualized yield (1.04 x 12). |

||||||||||||||

|

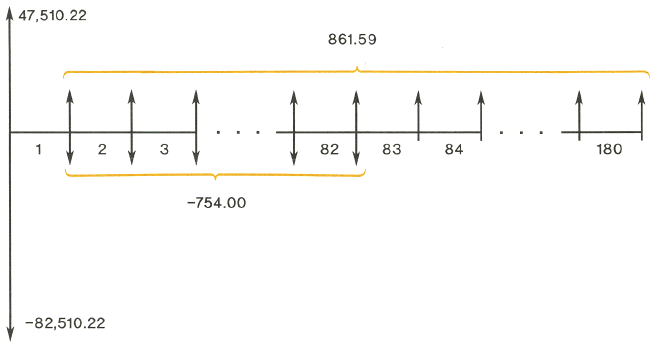

Wrap-Around Mortgages

A wrap-around mortgage is a combination of refinancing a mortgage and borrowing against real estate equity. Usually the two unknown quantities in the wrapped mortgage are the new payment and the rate of return to the lender. To arrive at a solution, you need to use both the TVM application and the cash-flow function IRR. Example: You have 82 monthly payments of $754 left on your 8% mortgage, leaving a remaining balance of $47,510.22. You would like to wrap that mortgage and borrow an additional $35,000 for another investment. You find a lender who is willing to "wrap" an $82,510.22 mortgage at 9.5% for 15 years. What are your new payments and what return is the lender getting on this wrap-around mortgage? The payment calculation is a straightforward TVM payment calculation using the new amount as the PV.

|

|||||||||||||||||||||||

C0 = 47,510.22 - 82,510.22 = -35,000.00

C1 = 861.59 - 754.00 = 107.59

N1 = 82

C2 = 861.59

N2 = 180 - 82 = 98

| Keys: | Display: | Description: |

| 35000 CHS g CF0 | -35,000.00 | Enters $35,000 for the loan amount. |

| RCL PMT CHS 754 - g CFj |

107.59 | Enters the net payment for the first 82 months. |

| 82 g Nj | 82.00 | Stores number of payments in this group. |

| RCL PMT CHS g CFj | 861.59 | Enters the net payment for the next 98 months. |

| 180 ENTER 92 - g Nj | 98.00 | Stores number of payments in group 2. |

| f IRR | 0.85 | Calculates the periodic return. |

| RCL g 12÷ | 10.16 | Recall the annual return. |